It’s unusual today to meet someone without any credit card debt. Whether you’re stuck making minimum payments while you watch your debts get higher every day, or you have a huge number of credit cards that you need to bring back under your control, there are many ways to lower your credit card debt and reign in your out-of-control finances.

It’s unusual today to meet someone without any credit card debt. Whether you’re stuck making minimum payments while you watch your debts get higher every day, or you have a huge number of credit cards that you need to bring back under your control, there are many ways to lower your credit card debt and reign in your out-of-control finances.

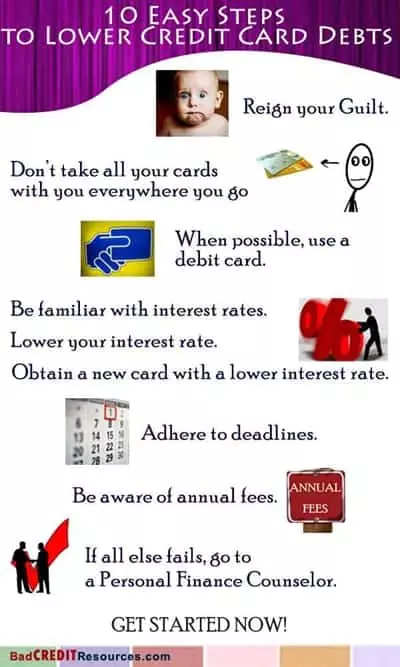

1. Reign in your guilt.

It’s tempting to beat yourself up over your debts and think the situation is futile, but doing so will keep you from taking steps to fix the problem. If you think you can’t find a solution, it’s easy to justify the “I can’t fix it, so I might as well break it further” line of thinking.

Share this Image On Your Site

It’s important to remember that no situation is completely hopeless. Taking the appropriate steps from the beginning will eventually lead to the eradication of debt.

2. Don’t take all your cards with you everywhere you go.

Rather than trying to maintain several credit card balances at once, keep one card (the one with the best rates and terms) in your wallet and store the rest at home or get rid of them entirely. This will make it easier to keep track of your spending and decrease your debt instead of adding to it.

3. When possible, use a debit card

Instead of pulling out your credit card when you’re short on cash, use your debit card instead. The money comes straight from your checking account, leaving no bill to pay and encouraging you to think twice before you spend money on something you might not need.

4. Be familiar with interest rates.

Interest rates on credit cards can be incredibly high, so a key component of lowering your debt is knowing how much interest you’re paying and how it affects the length of time it will take to pay off your credit card balance. This information can usually be found on your monthly statement.

5. Lower your interest rate.

Most credit card companies will be willing to lower your interest rate, especially if you indicate that you are willing to cancel your card and move to another company that offers lower rates.

6. Obtain a new card with a lower interest rate.

If your credit card company isn’t willing to lower your rate, consider transferring your balance to a lower-rate card. Be wary of “introductory rates,” however; they tend to end after six months or less, leaving you with a much higher rate.

7. Adhere to deadlines.

An important part of lowering credit card debt is paying close attention to payment deadlines. A late payment will often incur a fee of up to $25, making it harder to pay off your debt within your desired time frame. Consistent late payments can also negatively impact your credit score.

8. Be aware of annual fees.

You might be tempted to accept annual fees in exchange for a lower interest rate, but it’s not always worth it. Before choosing a credit card with an annual fee, do the math to make sure the fees will cost less than the potential accumulated interest.

9. If all else fails, go to a personal finance counselor.

Consumer credit counselors and debt management companies are there to help people who are truly in over their heads when it comes to their credit card debt. These kinds of services will teach you how to manage your spending and create a realistic payment plan. There are many reputable counselors and organizations that can help you eliminate your debt.

10. Get started now.

The hardest part of lowering credit card debt is getting the ball rolling. It’s tempting to say, “I’ll work on my spending and get serious about my debt tomorrow, but right now I really need this new shirt,” but that’s a self-defeating line of thought. There’s no time like the present to start; delaying will only allow the situation to grow further out of your control.

{kind=link}

This is all great advice. So many people I’ve come across seem to be having debt trouble. I think a part of it is that so many people weren’t given a proper education about finance by their parents.

Hi Inez, thanks for visiting! Yes I feel the same way. A lot of our clients tell me that their parents never really taught them the importance of saving for a rainy day! And to many of them grew up in families where a heavy debt load was considered normal. I hope that someday that will change!

These are great tips. Sharing this with my husband right now.

Hi Rachael,

Glad that you like our article! Share it to everyone please. 🙂

Thanks,

Shelly

Thanks to you guys for the helpful tips, I am in need of all the help I can get. I have two credit cards at the moment, one I use often the other not so much. I am thinking about just cancelling the one I don’t use often, or whichever one is better overall. I didn’t know that credit card companies will lower the interest rate, I’m going to try that soon and see what they say.

Thanks so much for the 10 steps. I have a decent amount of credit card debt that I could get through and I hope some of these steps can help me out in some way. Anyways, I appreciate all the information. Have a good day!

Hello Brad, thank you for visiting. Yes, it’s true; most of the credit card companies will be willing to lower your interest rate, especially if you indicate that you are willing to cancel your card.

Feel free to share it to your friends and family to know them how to lower their credit card debts. Thanks!

Shelly

Annual fees was one thing that got me when I first got my very first set of cards. I thought I wouldn’t have to pay anything else, but when I got my bill for the annual fee I was very annoyed. Now that I know, I always make sure to pay it as soon as possible. Otherwise I’m stuck with yet another bill.

Anyways, it gets easier when it comes to paying off credit card debts, it just takes time. That’s the big problem.

Number 8 has to be the most over looks thing with credit cards. Annual rates can be as low as 0 but as much as 400! So what is the point? To me, it is there way of saying your are going to use this card whether you need it or not! My second credit card was one of the $0 annual rates **FIRST YEAR***. I missed the first year part. Needless to say, I had a card with a limit of $500 and owed them $250 the next year. HALF of my limit. That is an example of a bad credit card.